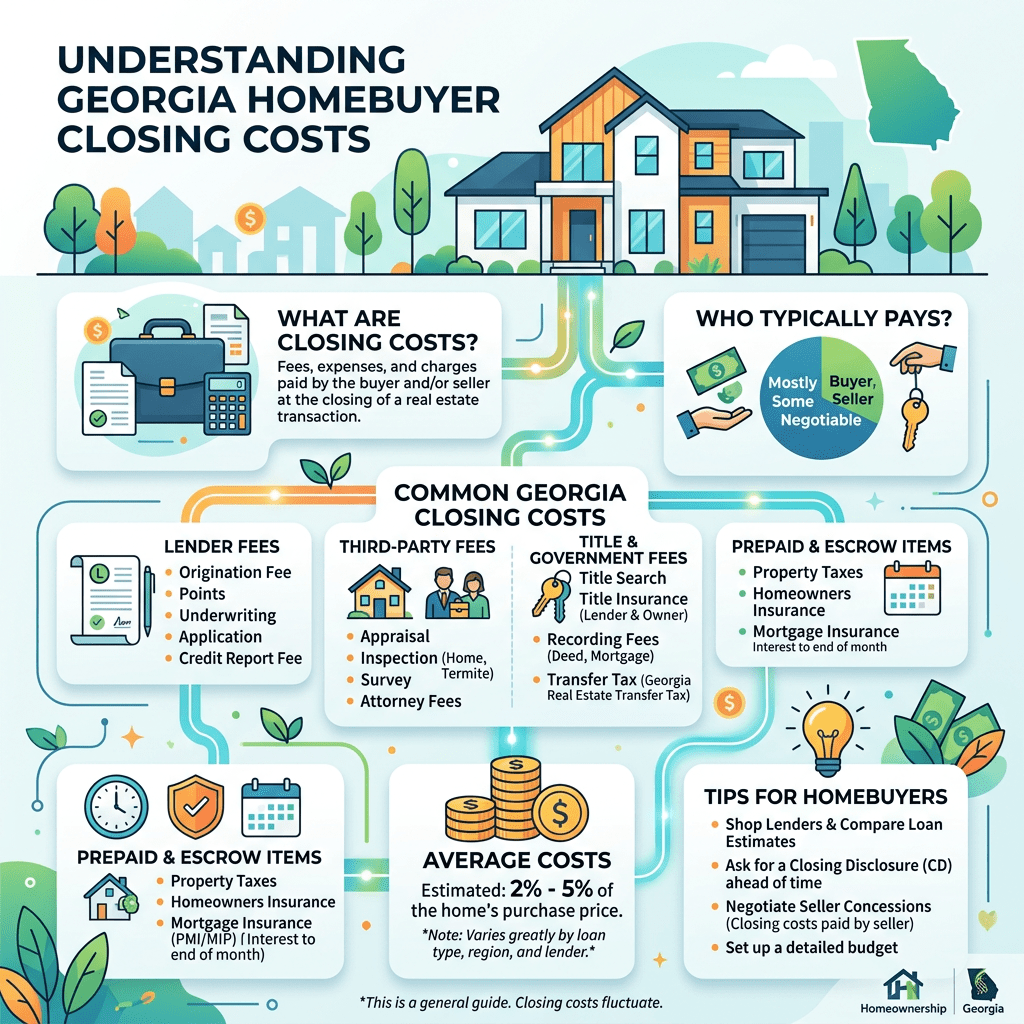

What are closing costs for homebuyers in Georgia? Closing costs for homebuyers in Georgia typically range from 2% to 5% of the loan amount and include lender fees, title insurance, attorney fees, prepaid taxes and insurance, and recording charges. On a $350,000 home in Coweta County, that could mean $7,000 to $17,500 due at closing — in addition to your down payment.

One of the most common questions I hear from buyers in Newnan and across Coweta County is some version of this: “I’ve saved for my down payment — but what else am I going to owe at closing?”

It’s a fair question, and it catches more buyers off guard than it should. Closing costs are real, they’re significant, and understanding them before you make an offer puts you in a much stronger position when it’s time to negotiate and close.

Georgia has a few specific rules that affect closing costs — particularly around attorney requirements — so if you’re relocating from another state, the process here may look a little different than what you’re used to. As a REALTOR® working with buyers throughout Coweta County, Newnan, Sharpsburg, Peachtree City, and the surrounding communities, I want to walk you through exactly what to expect.

What Are Closing Costs, and Why Do They Exist?

Closing costs are the fees and prepaid expenses required to finalize a home purchase. They cover the services, insurance, and government charges involved in transferring ownership from the seller to you.

Some of these costs are paid to third parties — your lender, the attorney, the title company, your insurance carrier. Others go directly to local and state government as required by law. None of them are negotiable in the sense that you can simply opt out — but some can be reduced, rolled in, or covered by the seller through negotiation.

Your lender is required by federal law to give you a Loan Estimate within three business days of your application, and a Closing Disclosure at least three business days before your closing date. Both documents itemize every cost — compare them carefully.

Georgia’s Attorney Requirement: What It Means for You

Georgia is an attorney-close state, which means a licensed real estate attorney must conduct your closing — this is non-negotiable.

Unlike many states where a title company alone handles closing, in Georgia the closing attorney manages the transfer of funds, conducts the title search, issues title insurance, handles disbursements, and files the deed with the county clerk. You’ll pay the closing attorney’s fee as part of your closing costs.

This is actually a buyer-friendly structure. Having a licensed attorney oversee your closing adds a meaningful layer of legal protection to the transaction. The closing attorney will file the deed with Coweta County records and ensure the title transfers cleanly.

If you’re relocating from a state that uses title companies only, this is an important distinction — and one more reason to work with a local REALTOR® who can guide you through the Georgia closing process from start to finish.

The Major Categories of Buyer Closing Costs in Georgia

Lender Fees

Your mortgage lender charges fees for originating and processing your loan. These typically include:

- Origination fee — charged by the lender for creating your loan, sometimes expressed as a percentage of the loan amount

- Underwriting fee — the cost of reviewing and approving your application

- Credit report fee — typically a minor charge passed through from the credit bureaus

- Discount points — optional; you pay upfront to buy down your interest rate

Getting loan estimates from two or three lenders before choosing is one of the most impactful financial decisions you can make as a buyer. Even a fraction of a percentage point in rate or fee difference adds up significantly over the life of a 30-year mortgage. The Consumer Financial Protection Bureau recommends comparing Loan Estimates from multiple lenders on the same day so rate comparisons are accurate.

Appraisal and Inspection Fees

Your lender will require a home appraisal to confirm the property is worth the purchase price before funding the loan. Appraisal fees are typically paid before closing — often when the appraisal is ordered — and are generally not refundable if the deal falls through.

A home inspection is separate from the appraisal and is not required by lenders, but it is strongly recommended. In Coweta County and across Georgia, buyers typically schedule the home inspection during the due diligence period after going under contract. This is your opportunity to understand the condition of the property before you’re fully committed.

Title Insurance

There are two types of title insurance, and they serve different purposes:

- Lender’s title insurance (required): Protects your lender if a title defect surfaces after closing.

- Owner’s title insurance (optional but recommended): Protects you as the buyer. If a title claim arises — a lien, an undisclosed heir, or a recording error — owner’s title insurance covers your legal defense and potential financial loss up to the coverage amount.

Owner’s title insurance is a one-time premium paid at closing and provides protection for as long as you own the home. Given the relatively modest cost, most experienced real estate advisors recommend carrying it.

Prepaid Items and Escrow Reserves

Prepaid costs are not fees — they’re expenses you’re paying in advance at closing:

- Homeowners insurance: Your lender typically requires you to prepay the first year’s policy at closing

- Prepaid mortgage interest: Interest that accrues from your closing date to the end of that month

- Property tax reserves: Your lender may require you to fund an escrow account with several months of property taxes at closing

- HOA fees: If the home is in a homeowners association in Coweta County, prorated dues may be due at closing

These items are real costs that would come due regardless — closing just front-loads them. First-time buyers in particular sometimes underestimate the total impact of prepaid items on what they need to bring to the closing table.

Recording Fees and Transfer Taxes

Georgia charges fees to record the deed and mortgage in the county real estate records. In Georgia, the intangibles tax on the mortgage is typically paid by the buyer, while the deed transfer tax is customarily paid by the seller — though this can be negotiated. Your closing attorney will handle all recording and filing with the Coweta County Clerk of Superior Court.

How Much Should You Budget for Closing?

As a rule of thumb, budget 2% to 5% of the loan amount for closing costs, in addition to your down payment. The range is wide because lender fees, the cost of owner’s title insurance, and prepaid amounts all vary based on your loan type, lender, and transaction specifics.

For homes in the mid-$300,000 range — a common price point across Coweta County, including communities in Newnan, Sharpsburg, and Grantville — closing costs often fall somewhere between $7,000 and $16,000. Freddie Mac confirms this 2%–5% range as the standard nationwide benchmark for most buyers. Your Loan Estimate from your lender will give you the precise figures for your specific transaction.

Don’t wait until the Closing Disclosure to understand your costs. Ask your lender to walk you through the Loan Estimate line by line as soon as you receive it. And lean on your REALTOR® — we review these documents regularly and can help you spot anything that warrants a closer look.

Can You Reduce or Offset Your Closing Costs?

Yes — and more buyers should ask about this. Here are the most common strategies used by buyers in Coweta County and Newnan:

- Negotiate seller concessions. In some market conditions, sellers will agree to contribute toward your closing costs as part of the purchase contract. This is more common when a home has had extended days on market or the seller is motivated to close on a specific timeline.

- Shop your lender. Lender fees are not standardized. Getting multiple Loan Estimates from different lenders on the same day allows for a true apples-to-apples comparison — and can reveal meaningful cost differences between options.

- Ask about closing cost assistance programs. The Georgia Dream Homeownership Program and other assistance programs may include closing cost assistance for qualifying buyers. Your lender can walk you through eligibility requirements.

- Understand what’s negotiable in your offer. Your REALTOR® can advise on what to request based on the specific property, the seller’s situation, and current market conditions across Coweta County.

Frequently Asked Questions: Closing Costs in Georgia

How much are closing costs when buying a home in Georgia?

Closing costs for Georgia homebuyers typically range from 2% to 5% of the loan amount. This includes lender fees, title insurance, the closing attorney’s fee, prepaid items like homeowners insurance and property taxes, and recording fees. Your lender is required to provide a Loan Estimate within three business days of your application, which will show your specific projected costs.

Do buyers or sellers pay closing costs in Georgia?

Both parties pay closing costs, but different ones. Buyers typically pay lender fees, title insurance, prepaid items, and attorney fees. Sellers typically pay the deed transfer tax and real estate commissions. In some transactions, a seller may agree to contribute toward buyer closing costs as a negotiated concession — your REALTOR® can advise on what’s reasonable to ask for based on current Coweta County market conditions.

Do I need a real estate attorney to close on a home in Georgia?

Yes. Georgia law requires that a licensed real estate attorney conduct the closing. The attorney manages the title search, issues title insurance, handles the transfer of funds, and files the deed with the county. The closing attorney’s fee is paid at closing and is included in your total closing costs.

Can I roll closing costs into my mortgage in Georgia?

In some cases, yes — depending on your loan type and lender. Some loan programs allow certain closing costs to be financed into the loan amount, which increases your loan balance and monthly payment. Ask your lender specifically what your loan program allows. Some programs also allow the seller to pay a portion of your closing costs as a negotiated concession at the time of the offer.

Let’s Talk Through Your Numbers

Understanding closing costs is one piece of a larger financial picture — and every buyer’s situation is a little different. If you’re planning to buy a home in Newnan, Coweta County, Peachtree City, or anywhere across South Metro Atlanta, we’re happy to walk you through what to expect at every stage of the process.

Call or text Mark Robertson at 678-763-0715, or reach the full R&R Team at randr.bhhsgeorgia.com. You can also email us at mark.robertson@bhhsgeorgia.com.

About the Authors: Mark & Jacqui Robertson are REALTORS® with the R&R Team at Berkshire Hathaway HomeServices Georgia Properties, serving buyers and sellers across Newnan, Coweta County, and the surrounding South Metro Atlanta area. With deep local roots and a combined background spanning real estate expertise and sales leadership, the R&R Team specializes in residential sales, relocation, new construction, and investment properties. Call or text 678-763-0715 or email mark.robertson@bhhsgeorgia.com.

All cost estimates are provided for general guidance and may vary based on your specific transaction, loan type, and lender. For a precise breakdown, consult your Loan Estimate from your lender.

Leave a comment